Global systemic crisis / Second half of 2012 — Convergence of four explosive factors: Banks-Stock Exchanges-Pensions-Debts

Whilst waiting for Euroland to equip itself, by the end of 2012, with a medium to long term common political, economic and social project, especially following the election of the new French president Francois Hollande, anticipated many months ago by LEAP/E2020, players will remain prisoners of the short-term reflexes related to the sudden Greek political tremors, the uncertainties over Euroland governance and to the risks in public debts.

At the same time, in the United States, the disappearance of the illusion of a recovery (1) combined with the renewal of concerns over the American financial sector's state of health (of which J P Morgan has just illustrated the fragility) and the big comeback of the country's debt problem is leading economic and financial players to contemplate an increasingly worrying future (2).

In the United Kingdom, the country's return to recession is combining with the failure to control deficits and the rise of working-class anger in the face of an austerity which has however only just begun (3).

In Japan, economic sluggishness and the weakening of exports in a context of world recession (4) have brought the spectrum of the country's excessive debt back to the surface.

In this context, according to LEAP/E2020, the second half of 2012 will be the preferred moment for the convergence of four explosive factors for the Western economies: banks, stock exchanges, pensions and debts.

For economic, financial or political players as for simple households, this convergence will cause major risks to weigh on the state of their finances as well as on their aptitude to face the challenges to come.

Therefore, in this GEAB issue our team expands on its anticipations concerning these four explosive factors of the second half of 2012 as well as the recommendations to minimize their negative consequences. In addition, LEAP/E2020 sets out its new anticipation on the global systemic crisis' consequences as regards international languages (on a world level and in Europe) out to 2030 in order to help parents and children, as well as teaching institutions, make the correct language learning choices today.

In this GEAB N°65 press release, our team has chosen to introduce the explosive factor relating to public and private debt

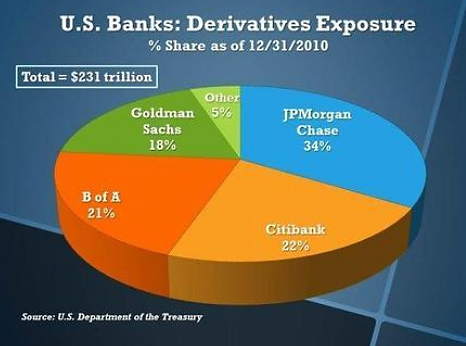

US banks' derivatives exposure at 31/12/2010 - Sources: Dpt of Treasury/Mybudget360, 11/2011

Debts: difficult to manage sovereign debt and deadly private debt… creditors painfully approach the day of reckoning and people an explosion of anger

LEAP/E2020 announced it in 2008 and repeated it many times since. There was approximately 30 trillion USD of phantom assets in the world financial system of which about 15 trillion USD remains, which will mostly fly off by the end of 2012. The good news is that as from then, one can seriously contemplate the rebuilding of a healthy world financial system. The bad news is that is during the quarters to come this 15 trillion USD will go up in smoke. That implies, of course, as we have previously suggested, the bankruptcy (and/or rescue by the States) of 10% to 20% of Western banks. And this time, unlike 2008/2009, the shareholders will be the first victims (including in the United States), whatever the priority of their rights (5). Only shareholders carrying significant geopolitical weight will be treated with consideration (sovereign funds, friendly States…).

As regards private debts, households will mainly, in particular in the United States and the United Kingdom, have to face the consequences of the increase in the resulting insolvency rates which will affect them on their own. Caught in the trap of austerity and recession, the Western States no longer have the wherewithal to help the middle class as long as growth hasn't picked up a little bit. And sadly, that won't be the case by the end of 2012. Moreover, in the United States one is currently seeing the student debt issue in the process of turning itself into a “subprime encore” (6). Increasing fees due to the end of a Federal state grants policy and political paralysis in Washington against attempts to control the federal deficit are in the process of creating a disaster for millions of young Americans and their parents.

In Europe, the United Kingdom has already decided to let its middle class face its record debt alone. That comes down to causing it to fall into the underprivileged class. The next few months will see a new sudden confrontation between this British middle class and its leaders almost exclusively belonging to the upper-class.

On the continent, via votes rejecting leaders who were disciples of austerity as the one and only solution to the public debt crisis, the people have opened a major democratic confrontation with the elite in place for nearly twenty years, and at creditors' beck and call. The attempt which personifies the new French president, Francois Hollande, to open a middle way between austerity and Keynesian reflation which have both failed or are impossible politically or budget-wise, will succeed (because it's the only politically and budgetary viable one from now on (7)) but not before the end of 2012 (8).

Meanwhile, sudden political tremors as in Greece and complex negotiations at Euroland's core will dominate the agenda, making creditors and their exhalation, and the markets increasingly nervous (9). And this market nervousness is heightened by the awareness of the infinite brittleness of the Wall Street and City financial institutions vis-a-vis the risk of non-repayment of debts: national or private. They are almost the last assets on their balance sheet from which they still hope to be able to recover significant value.

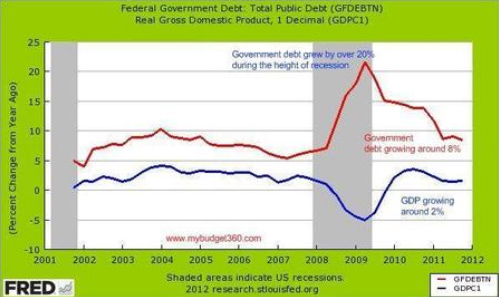

US Federal Government Debt and GDP compared (2001-2012) (in red: debt/in blue: GDP - Source: StLouisFed / Mybudget360, 04/2012

From the end of summer 2012, the return of the topic of the United States' unmanageable debt, related to the automatic budget reductions imposed in the event of Congress' non-agreement on debt reduction, will start a “Taxmageddon (10) » in the USA. One will thus witness the remake of the detonator-bomb tandem that European and American debts already played with in summer 2011, but this time in a much more powerful version. In fact, if fears of seeing the Euro and Euroland exploding have disappeared (11), they will be replaced by a danger much more alarming to the markets: the massive and sudden monetization of US debt (12).

In addition, this situation will show up in the United States in a context of complete political paralysis (13), with a Congress partitioned by the emergence of radical factions in the Republican (“Tea-Party”) as well as the Democrat party (“Occupy Wall Street”) (14).

--------

Notes :

(1) A recovery so illusory that it has given rise to a return to “subprime” practices. And even the price of milk, a reliable signal of economic slowdown, points towards recession. Sources: CNBC, 26/04/2012 ; New York Times, 10/04/2012

(2) On this subject, remember that the US government and the Fed must now create 2.5$ of debt to generate 1$ of growth. It's the problem which any economy whose debt becomes excessive meets. It's the kind of “detail” that Keynesians like Krugman forget to mention when they indiscriminately claim that austerity policies are absurd. As for any common sense approach, which takes the real world into account and not economic theories, a balance is needed between debt reduction and the support of growth. It is, moreover, the path which Euroland will take as of this summer; whereas the United States continues to deny the need to deal with their runaway debt.

(3) Source: WallStreetJournal, 13/05/2012

(4) Sources: TimesofIndia, 11/05/2012; MarketWatch, 10/05/2012; ChinaDaily, 06/05/2012; ChinaDaily, 28/03/2012; Washington Post, 11/05/2012 ; USAToday, 13/04/2012; CNBC, 06/04/2012

(5) Source: MarketWatch, 10/05/2012

(6) Source: CERF, 21/04/2012

(7) Since February 2012 and the GEAB N°62, our team set out its anticipation on Euroland 2012-2016 in detail and the events in progress confirm it to us in our analysis (if you wish to have a “live” presentation of Euroland and Europe's prospects, you can also take a look at Franck Biancheri speech in English on the 2nd May to 1,000 delegates of the principal European student network AEGEE-EUROPE). By this summer, after the June 2012 French legislative elections, a six-handed agreement on a austerity/growth balance will be found (France/Germany/Italy/Netherlands/Belgium/Spain) which will be carried out by Euroland+ (Euroland plus the other countries involved in the EMS).

(8) In Germany also increasingly numerous and loud voices are demanding a more balanced way because the social costs of German economic success are starting to increasingly weigh on a growing part of the population. Source: Spiegel, 04/05/2012

(9) For example, the Norwegian sovereign fund has decided to dispose of its sovereign debt assets in the weak Euroland countries. However, with regard to the Euro, LEAP/E2020 points out that there is no reason to worry and, on the contrary, by the end of 2012 it's the US Dollar which will account for the downwards shock. Sources: LeFigaro, 05/05/2012; MarketWatch, 09/05/2012

(10) A buzz word created from the two words “Tax” and “Armageddon”. It indicates the tax chaos which will reign at the end of 2012 at the time when choices for massive budgetary cuts in the US federal budget will be required. For nearly a year, the United States and the international financial press have chosen to carefully ignore this major problem. It will only be more difficult to manage when it makes its presence felt on the landscape again.

(11) As we underlined last January, it's one of the big differences between the current Greek crisis and the anti-Euro hysteria of 2010/2011. If, today, it's theoretically possible to consider Greece exiting Euroland without a questioning of the single currency, the fact remains that in reality such an exit is impossible. Besides it's one of the problems with which the Greek leaders are confronted. We emphasise this point to recall that on this subject economists, who live in theoretical worlds with little or no relationship to reality, have been constantly wrong for months. The champions of the end of the Euro, from Krugman to Roubini, have as much credibility on the matter as the Roman haruspices which divined the future from animals' entrails. To return to Greece, LEAP/E2020 takes the view that whilst the leaders of the two major government parties (PASOK and ND) belong to the generation which led the country into this historic crisis, there will be no viable political exit absent popular confidence… Therefore, it's for the Euroland leaders, and in particular Angela Merkel via the EPP and Francois Hollande via the PES, to put pressure on their respective “parties-in-arms” so that by September 2012 and the next elections, the whole leadership of these two parties are replaced by one less than 45 years old. The current success of the extreme-left Syrisa party is due as much to its ideas as at the age of its leader: 38. A process of this type has been used to manage to get an end of the road Silvio Berlusconi to give up power. The means thus exist. And whilst on the subject, it's a question of making it possible for the Greeks to find confidence in new leaders, from the right or left, inclusive. To really understand why a Greek Eurozone exit is impossible in practice, only one example is needed: if you were Greek, and it was suggested that you exchange your Euros for new Drachmas, what would you do? No comment!

(12) Even the former US Treasury Secretary Robert Rubin has now joined the chorus of those who warn of this serious risk in the short-term. Source: Reuters, 10/05/2012

(13) Whether it is Barack Obama or Mitt Romney who wins the presidential election.

(14) See GEAB N°60

Mercredi 16 Mai 2012